Blockchain vs Networked Accounting Ledgers

Why Smart Contracts Fall Short

)

William Pallumbo

Deployment Manager - TapestryX

Introduction

Why Smart Contracts Fall Short

Blockchain is seen as a technology of the future, yet it forgot to include the future in its ledger. In this article, we will compare the functionality of traditional blockchains to the next-generation Networked Accounting Ledger (NAL).

Forgetting the Future: The Limited Functionality of Current Blockchains

The advent of the blockchain spawned multiple public and private chains hoping to take advantage of the technology’s peer-to-peer and rapid settlements, and the ability to tokenize and settle any asset within the same protocol. However, the blockchains could (and largely still can) only record transfers of currently held assets (i.e., long positions). Transactions involving future obligations (i.e., payables and receivables) are currently not able to be recorded on-chain. To overcome this fundamental deficiency, so-called smart-contracts were introduced to encode them off-chain with if/then/else executable lines of code to post them when they came due.

Although these smart contract “codelets” may be effective for transferring assets at a future date, they do not provide an acceptable way to accrue, project or reconcile. The blockchain ledger does not reveal the “future” transfer until it is a “current date” transfer.

Standard Accounting practices include double entry accounting and the concept of transacting periods and future-dated obligations (recorded as payables by one party and receivables by the counterparty). So, upon having a future-dated obligation, it can be recorded to both ledgers as such and can be accrued, projected and reconciled.

Without the future-dated payables and receivables - pending trades, pending dividends and interest or loaned securities or cash - any fund or institution’s balance sheet cannot be correctly valued.

Why Future-Dated Transactions Are Critical in Finance

In institutional finance, transactions are executed in multiple currencies and securities that may not be currently held in inventory at the time of the transaction. For example: a bank lends its deposits. Therefore, any new payments in or out or any new or closed loans affect the balance of funds the bank can further lend or needs to borrow. A broker will trade securities that it can buy/sell, borrow or lend for financing or different trading strategies. These settlements are almost never settled individually, in what is known as real-time gross settlement (RTGS),- as the balances of securities or cash cannot be projected against trades that are not known until they are executed. With, and only with the proper recording of future-dated payables and receivables can the required positions be projected, netted and financed or sourced before settlement.

The Hidden Risks and Inefficiencies of Smart Contracts

Another aspect of smart contracts is that they are disclosed to the network and must be run by the protocol validators to be accepted into the distributed ledger. This raises two other issues:

The smart contracts redundantly recreate the logic and conditions already managed within the trading, risk, credit and order/execution management systems (OMS/EMS). There is also the potential for the smart contract code to be wrong or use different data from independent sources.

The disclosure of the smart contracts to the network not only undermines the confidentiality of the transacting parties, it has allowed front running, spoofing and transaction hacking with crypto currency decentralized finance (DeFi).

In summary, current blockchains are perpetual, continuous state change (asset transfer) logs, which do not have the three critical properties of:

The means to record double accounting entries in the ledger;

Distinct, reconcilable and archivable transacting periods and

A visible recording of future-dated obligations

Because current blockchains rely on smart contracts to record future obligations, they are ineffective from an accounting perspective, and will never be able to handle the dynamic financing needs of institutional banking and capital markets.

What Is a Networked Accounting Ledger (NAL) and How It Solves Blockchain’s Limitations

For a blockchain/DLT to be effective for institutional banking and capital markets, it needs to be a Networked Accounting Ledger (NAL). The NAL uses double-entry accounting across nodes and counterparties to accrue, net, and finance positions. It records transactions in a way that is immediately consumable by legacy systems, because it “talks” in the standard, international business language of debits and credits.

L4S Corp.’s TapestryX is a production ready, B2B optimized NAL

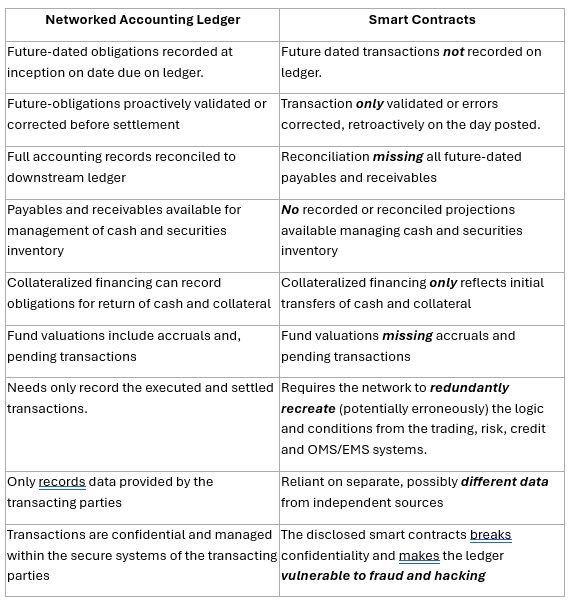

Below is a side-by-side comparison of a NAL vs Smart Contracts:

Download the Pyaza app to follow our coverage, connect with the team and get involved in upcoming creator campaigns.

'%3e%3cpath%20fill='%23000'%20d='M0%200h135v40H0z'/%3e%3cpath%20d='M47.45%2010.24c0%20.84-.25%201.51-.75%202-.56.59-1.29.89-2.2.89-.91%200-1.61-.3-2.21-.9-.6-.6-.9-1.35-.9-2.23%200-.88.3-1.63.9-2.23.6-.6%201.34-.91%202.21-.91.44%200%20.86.08%201.25.23.39.16.71.38.96.66l-.55.55c-.18-.22-.42-.4-.72-.52a2.29%202.29%200%2000-.94-.19c-.65%200-1.21.23-1.66.68-.45.46-.67%201.03-.67%201.72s.22%201.26.67%201.72c.45.45%201%20.68%201.66.68.6%200%201.09-.17%201.49-.5.4-.33.63-.8.69-1.38H44.5v-.72h2.91c.03.16.04.31.04.45zM52.06%207v.74h-2.73v1.9h2.46v.72h-2.46v1.9h2.73V13h-3.5V7h3.5zm3.25.74V13h-.77V7.74h-1.68V7h4.12v.74H55.3h.01zM60.74%2013h-.77V7h.77v6zm3.42-5.26V13h-.77V7.74h-1.68V7h4.12v.74h-1.68.01zM74.52%2010c0%20.89-.3%201.63-.89%202.23-.6.6-1.33.9-2.2.9-.87%200-1.6-.3-2.2-.9-.59-.6-.89-1.34-.89-2.23%200-.89.3-1.63.89-2.23.59-.6%201.32-.91%202.2-.91.88%200%201.6.3%202.2.91.59.6.89%201.34.89%202.22V10zm-5.38%200c0%20.69.22%201.27.65%201.72.44.45.99.68%201.64.68.65%200%201.2-.23%201.63-.68.44-.45.66-1.02.66-1.72s-.22-1.27-.66-1.72c-.44-.45-.98-.68-1.63-.68-.65%200-1.2.23-1.64.68-.44.45-.65%201.03-.65%201.72zm7.23%203h-.77V7h.94l2.92%204.67h.03l-.03-1.16V7h.77v6h-.8l-3.05-4.89h-.03l.03%201.16v3.74l-.01-.01zm-8.2%208.75c-2.35%200-4.27%201.79-4.27%204.25s1.92%204.25%204.27%204.25c2.35%200%204.27-1.8%204.27-4.25s-1.92-4.25-4.27-4.25zm0%206.83c-1.29%200-2.4-1.06-2.4-2.58s1.11-2.58%202.4-2.58c1.29%200%202.4%201.05%202.4%202.58s-1.11%202.58-2.4%202.58zm-9.31-6.83c-2.35%200-4.27%201.79-4.27%204.25s1.92%204.25%204.27%204.25c2.35%200%204.27-1.8%204.27-4.25s-1.92-4.25-4.27-4.25zm0%206.83c-1.29%200-2.4-1.06-2.4-2.58s1.11-2.58%202.4-2.58c1.29%200%202.4%201.05%202.4%202.58s-1.11%202.58-2.4%202.58zm-11.08-5.53v1.8h4.32c-.13%201.01-.47%201.76-.98%202.27-.63.63-1.61%201.32-3.33%201.32-2.66%200-4.74-2.14-4.74-4.8%200-2.66%202.08-4.8%204.74-4.8%201.43%200%202.48.56%203.25%201.29l1.27-1.27c-1.08-1.03-2.51-1.82-4.53-1.82-3.64%200-6.7%202.96-6.7%206.61%200%203.65%203.06%206.61%206.7%206.61%201.97%200%203.45-.64%204.61-1.85%201.19-1.19%201.56-2.87%201.56-4.22%200-.42-.03-.81-.1-1.13h-6.07v-.01zm45.31%201.4c-.35-.95-1.43-2.71-3.64-2.71s-4.01%201.72-4.01%204.25c0%202.38%201.8%204.25%204.22%204.25%201.95%200%203.08-1.19%203.54-1.88l-1.45-.97c-.48.71-1.14%201.18-2.09%201.18s-1.63-.43-2.06-1.29l5.69-2.35-.19-.48h-.01zm-5.8%201.42c-.05-1.64%201.27-2.48%202.22-2.48.74%200%201.37.37%201.58.9l-3.8%201.58zm-4.62%204.12h1.87v-12.5h-1.87v12.5zm-3.06-7.3h-.06c-.42-.5-1.22-.95-2.24-.95-2.13%200-4.08%201.87-4.08%204.27%200%202.4%201.95%204.24%204.08%204.24%201.01%200%201.82-.45%202.24-.97h.06v.61c0%201.63-.87%202.5-2.27%202.5-1.14%200-1.85-.82-2.14-1.51l-1.63.68c.47%201.13%201.71%202.51%203.77%202.51%202.19%200%204.04-1.29%204.04-4.43V22h-1.77v.69zm-2.14%205.88c-1.29%200-2.37-1.08-2.37-2.56s1.08-2.59%202.37-2.59%202.27%201.1%202.27%202.59c0%201.49-1%202.56-2.27%202.56zm19.91-11.08v12.5h1.87v-4.74h2.61c2.07%200%204.1-1.5%204.1-3.88s-2.03-3.88-4.1-3.88h-4.48zm4.52%206.03h-2.65v-4.29h2.65c1.4%200%202.19%201.16%202.19%202.14%200%20.98-.79%202.14-2.19%202.14v.01zm11.53-1.8c-1.35%200-2.75.6-3.33%201.91l1.66.69c.35-.69%201.01-.92%201.7-.92.96%200%201.95.58%201.96%201.61v.13c-.34-.19-1.06-.48-1.95-.48-1.79%200-3.6.98-3.6%202.81%200%201.67%201.46%202.75%203.1%202.75%201.25%200%201.95-.56%202.38-1.22h.06v.96h1.8v-4.79c0-2.22-1.66-3.46-3.8-3.46l.02.01zm-.23%206.85c-.61%200-1.46-.31-1.46-1.06%200-.96%201.06-1.33%201.98-1.33.82%200%201.21.18%201.7.42a2.254%202.254%200%2001-2.22%201.98v-.01zm10.58-6.58l-2.14%205.42h-.06l-2.22-5.42h-2.01l3.33%207.58-1.9%204.21h1.95l5.13-11.79h-2.08zm-16.81%208h1.87v-12.5h-1.87v12.5z'%20fill='%23fff'/%3e%3cpath%20d='M20.75%2019.42L10.1%2030.72a2.876%202.876%200%20004.24%201.73l.03-.02%2011.98-6.91-5.61-6.11.01.01z'%20fill='%23EA4335'/%3e%3cpath%20d='M31.52%2017.5h-.01l-5.17-3.01-5.83%205.19%205.85%205.85%205.15-2.97a2.88%202.88%200%20001.51-2.53c0-1.09-.6-2.04-1.5-2.52v-.01z'%20fill='%23FBBC04'/%3e%3cpath%20d='M10.1%209.28c-.06.24-.1.48-.1.74v19.96c0%20.26.03.5.1.74l11.01-11.01L10.1%209.28z'%20fill='%234285F4'/%3e%3cpath%20d='M20.83%2020l5.51-5.51-11.97-6.94a2.89%202.89%200%2000-4.27%201.72l10.73%2010.72V20z'%20fill='%2334A853'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_204_2'%3e%3cpath%20fill='%23fff'%20d='M0%200h135v40H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)