Improving Stablecoins with TapestryX NaL (Part3)

How TapestryX compares to traditional blockchain systems, highlight findings from the ISSA report, and explore the global regulatory landscape in more detail.

)

William Pallumbo

Deployment Manager - TapestryX

Introduction

How TapestryX compares to traditional blockchain systems, highlight findings from the ISSA report, and explore the global regulatory landscape in more detail.

TapestryX NAL vs DLTs w/ smart contracts

Current Blockchain Solutions

No Accounting

Time-stamped (state change log) transfers only

Continuous expanding active memory

No record of future obligations

Smart contracts used to record future obligations introduce significant operational and accounting challenges.

Latency – delay in settlement

Mining, Consensus or Validators

Limited Performance

Not Scalable

Finite or diminishing capacity

Limited to no interoperability with legacy infrastructure/other networks

Difficult adoption & transition

Customized (Unique Smart Contracts per use-case transaction)

Networked Accounting Ledger Technology (NAL)

Double-Entry Accounting

Transacting periods

Archived transaction periods

Future-dated obligations *

Accounting-format, reconcilable future obligations’ records for downstream G/L, Risk or Credit applications

Real-time

Self-synchronizing DLT *

High Performance

Linearly Scalable *

High-Capacity

Interoperable with Legacy Infrastructure or other networks

Implement at large or small scale

No-code, asset/life-cycle configurable *

*U.S. Pat. No. 11,631,063 B2

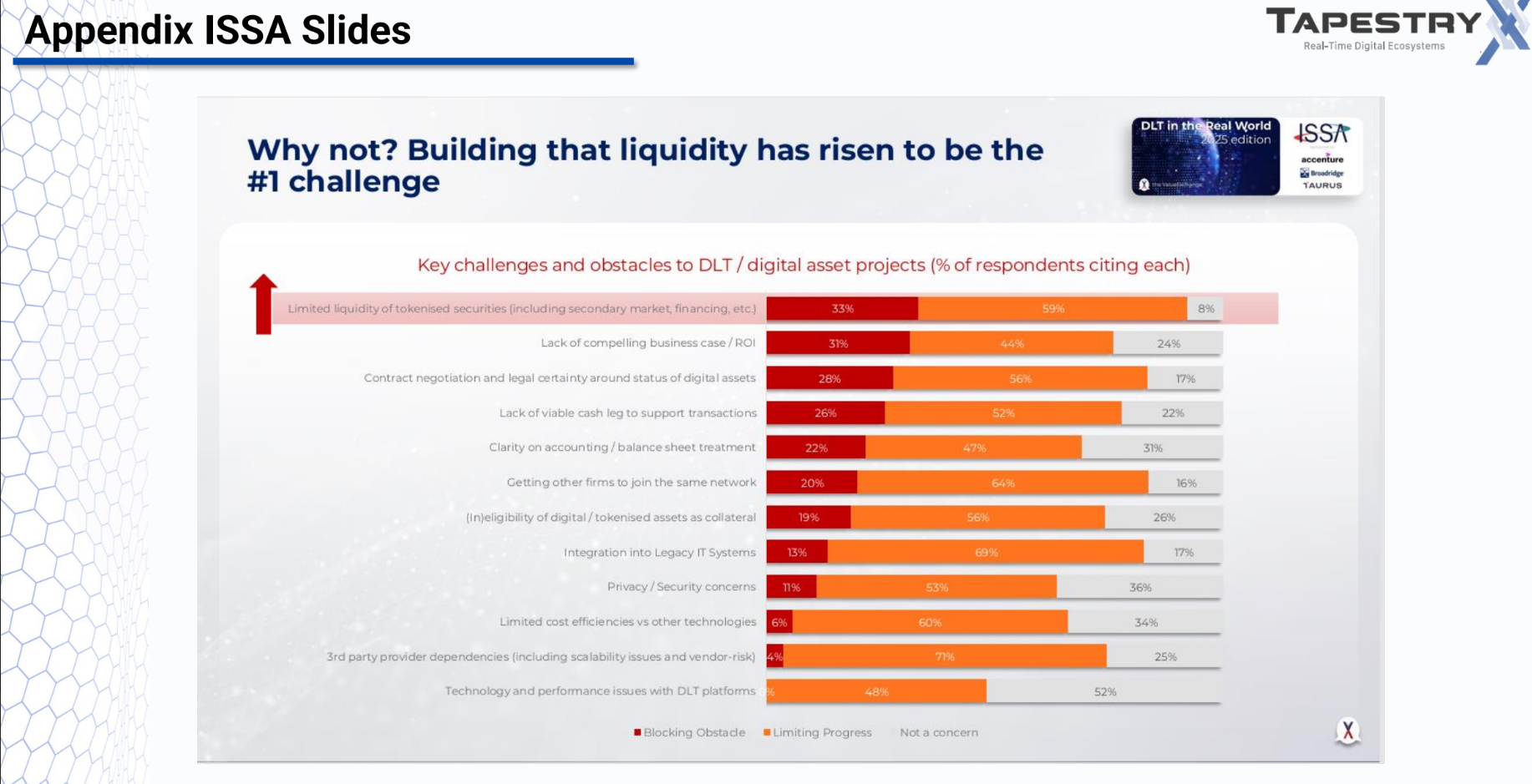

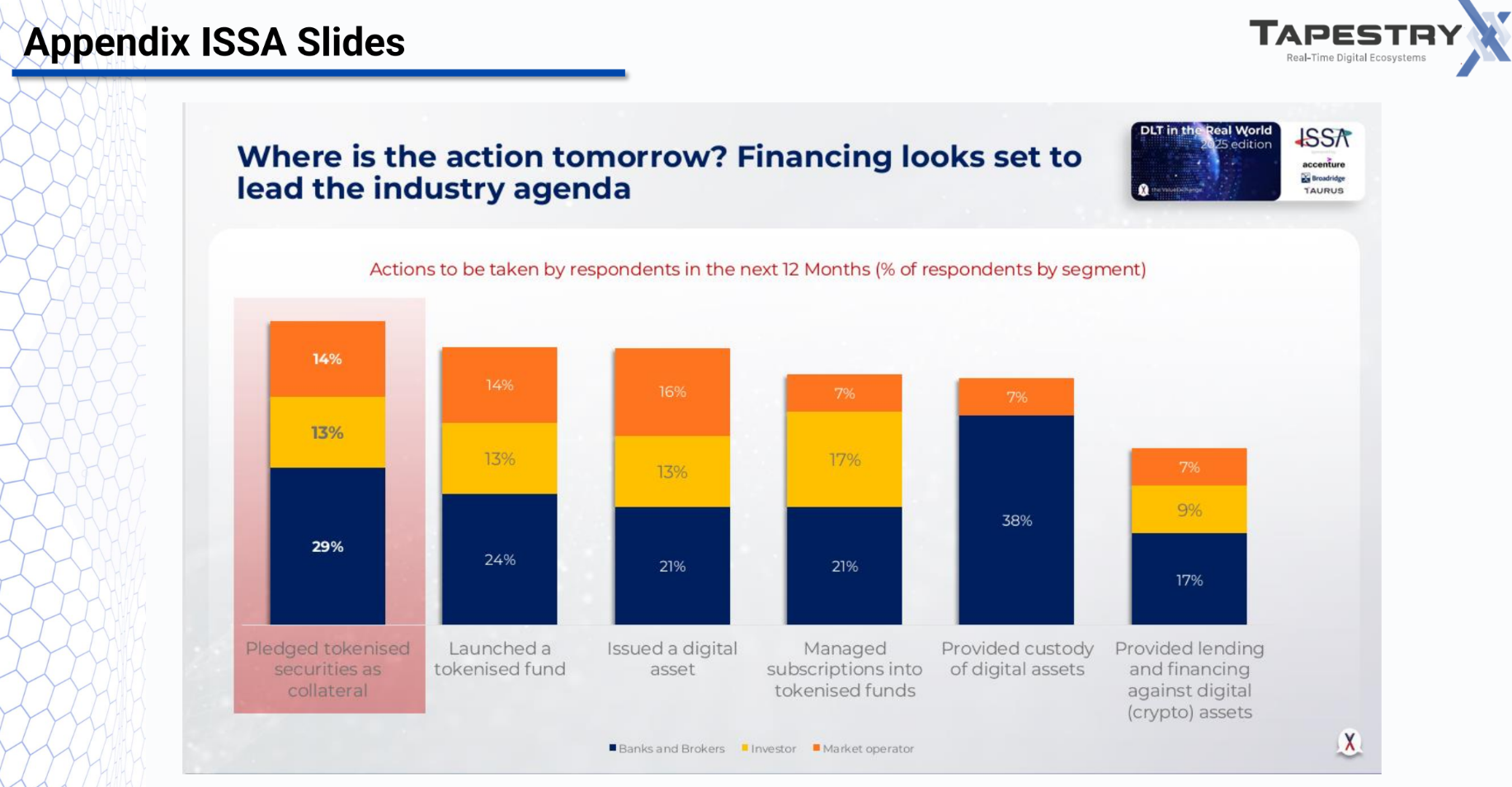

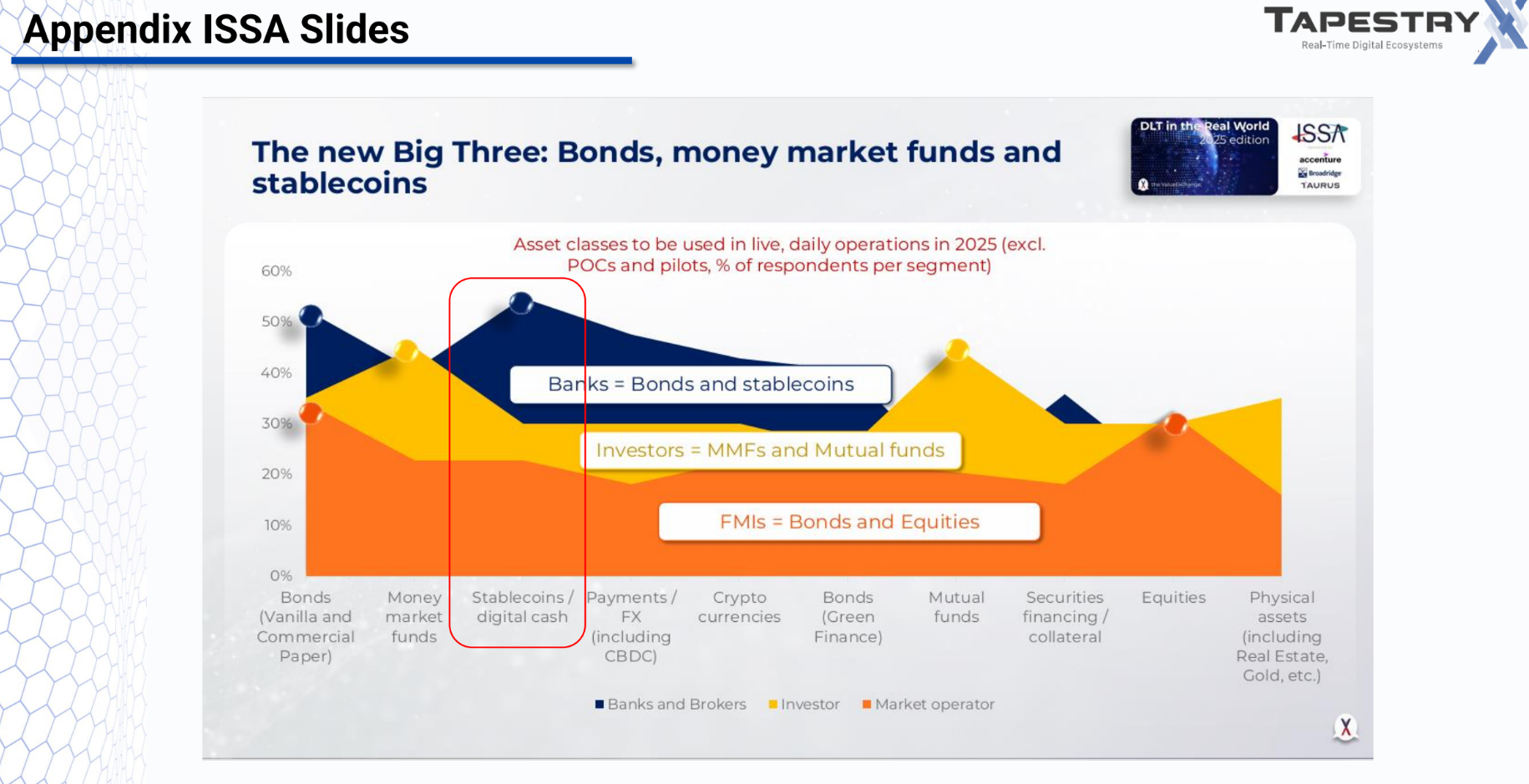

APPENDIX ISSA SLIDES

Regulatory Details

United States

Federal landscape

No unified “stablecoin law”; STABLE Act (House) and GENIUS Act (Senate) pending

Issuers rely on MSB/money-transmitter rules, Bank Secrecy Act, state-by-state licensing or bank charter

Key constraints

Only depository institutions can self-issue

Nonbank issuers must partner with banks or register as money transmitters (meeting reserve and audit obligations)

State regimes

New York BitLicense, Wyoming stablecoin law, etc.

1:1 reserve requirements, licensing fees, periodic audits, capital/insurance minimums

Varying rules on redemption rights, eligible collateral, permissible APYs

BIS Report: https://www.bis.org/publ/arpdf/ar2025e3.pdf

European Union (MiCA)

Effective June 2024 under Markets in Crypto-Assets Regulation

Issuer obligations

Maintain 1:1 High-Quality Liquid Asset reserves

Guarantee daily redemptions at face value

Obtain an “electronic money token” (EMT) license under the e-money directive

Ongoing duties

Monthly disclosures, strict AML/KYC, adverse-event reporting

Cross-border passporting across all 27 member states

United Kingdom

E-money treatment under FCA’s Electronic Money Institution (EMI) regime

Core requirements

Safeguard 100 percent of customer funds in ring-fenced accounts

Robust governance, conduct rules, and capital buffers

Innovation hub

Temporary registration with lighter touch

Caps on AUM and geographic reach

Singapore

Payment Services Act classifies stablecoins as “designated payment tokens”(DPTs)

Major Payment Institution lice nse

1:1 segregated reserves in MAS-licensed banks

Quarterly audits, stringent AML/CFT controls, local board representation

Regional access via APEC and ASEAN passporting agreements

Hong Kong

Stablecoin Bill (anticipated 2025)

Licensing via HKMA as a stored-value facility

Issuer duties

Reserve holdings in HQLA or on-demand bank deposits

HK$ redemptions within 24 hours

Monthly reports and independent proof-of-reserves

Switzerland

FINMA classification: stablecoins are “payment tokens”

Dual regimes

Payment system with multilateral settlement (for banking-level issuers)

Financial intermediary rules (lighter compliance, limited KYC/AML)

Reserves calibrated to expected daily transaction volumes

Cayman Islands

Virtual Asset Service Provider (VASP) Law

Issuer requirements

Register as a VASP, maintain 100 percent backing, annual audits

Capital buffer tied to a percentage of AUM

Redemption mechanism via contractual rights rather than on-shore guarantees

Dubai (DFSA)

Crypto Tokens regime (since 2024)

Tier 1 (banks, licensed custodians): unlimited issuance & market-making

Tier 2 (fintechs): issuance caps based on AUM

Both tiers require client asset segregation, 1:1 reserves, KYC/AML, monthly reporting

Bermuda

Digital Asset Business Act

Key rules

100 percent backing held in segregated trust accounts

Oversight as a trust company, quarterly attestations

On-chain proof-of-reserves

Malaysia

Securities Commission framework

Only licensed banks or approved e-wallet operators may issue

Must safeguard client funds, meet capital adequacy, conduct quarterly audits, and enforce KYC/AML

Interest on Stablecoins

General prohibition on paying interest/yield directly in the token to avoid securities classification

Permitted structures (some US states, Cayman)

Interest issued via separate contracts, no on-chain markup

Additional capital or surety to cover credit risk

Platform requirements

US: broker-dealer or securities registration

EU/HK: asset management or specific yield-product licensing

Transparency mandates: disclose NAV, lock-up periods, fees, counterparty exposures

DeFi-style permissionless yield remains off-limits in regulated frameworks

Looking Ahead: Key Developments to Watch

Global coordination on a unified stablecoin standard (BIS, FSB initiatives)

Regulatory clarity around algorithmic and crypto-collateralized stablecoins

Integration of programmable compliance features (on-chain audit trails, real-time reserve proofs)

Convergence between stablecoins and retail CBDCs for cross-border interoperability.

Download the Pyaza app to follow our coverage, connect with the team, and get involved in upcoming creator campaigns.

'%3e%3cpath%20fill='%23000'%20d='M0%200h135v40H0z'/%3e%3cpath%20d='M47.45%2010.24c0%20.84-.25%201.51-.75%202-.56.59-1.29.89-2.2.89-.91%200-1.61-.3-2.21-.9-.6-.6-.9-1.35-.9-2.23%200-.88.3-1.63.9-2.23.6-.6%201.34-.91%202.21-.91.44%200%20.86.08%201.25.23.39.16.71.38.96.66l-.55.55c-.18-.22-.42-.4-.72-.52a2.29%202.29%200%2000-.94-.19c-.65%200-1.21.23-1.66.68-.45.46-.67%201.03-.67%201.72s.22%201.26.67%201.72c.45.45%201%20.68%201.66.68.6%200%201.09-.17%201.49-.5.4-.33.63-.8.69-1.38H44.5v-.72h2.91c.03.16.04.31.04.45zM52.06%207v.74h-2.73v1.9h2.46v.72h-2.46v1.9h2.73V13h-3.5V7h3.5zm3.25.74V13h-.77V7.74h-1.68V7h4.12v.74H55.3h.01zM60.74%2013h-.77V7h.77v6zm3.42-5.26V13h-.77V7.74h-1.68V7h4.12v.74h-1.68.01zM74.52%2010c0%20.89-.3%201.63-.89%202.23-.6.6-1.33.9-2.2.9-.87%200-1.6-.3-2.2-.9-.59-.6-.89-1.34-.89-2.23%200-.89.3-1.63.89-2.23.59-.6%201.32-.91%202.2-.91.88%200%201.6.3%202.2.91.59.6.89%201.34.89%202.22V10zm-5.38%200c0%20.69.22%201.27.65%201.72.44.45.99.68%201.64.68.65%200%201.2-.23%201.63-.68.44-.45.66-1.02.66-1.72s-.22-1.27-.66-1.72c-.44-.45-.98-.68-1.63-.68-.65%200-1.2.23-1.64.68-.44.45-.65%201.03-.65%201.72zm7.23%203h-.77V7h.94l2.92%204.67h.03l-.03-1.16V7h.77v6h-.8l-3.05-4.89h-.03l.03%201.16v3.74l-.01-.01zm-8.2%208.75c-2.35%200-4.27%201.79-4.27%204.25s1.92%204.25%204.27%204.25c2.35%200%204.27-1.8%204.27-4.25s-1.92-4.25-4.27-4.25zm0%206.83c-1.29%200-2.4-1.06-2.4-2.58s1.11-2.58%202.4-2.58c1.29%200%202.4%201.05%202.4%202.58s-1.11%202.58-2.4%202.58zm-9.31-6.83c-2.35%200-4.27%201.79-4.27%204.25s1.92%204.25%204.27%204.25c2.35%200%204.27-1.8%204.27-4.25s-1.92-4.25-4.27-4.25zm0%206.83c-1.29%200-2.4-1.06-2.4-2.58s1.11-2.58%202.4-2.58c1.29%200%202.4%201.05%202.4%202.58s-1.11%202.58-2.4%202.58zm-11.08-5.53v1.8h4.32c-.13%201.01-.47%201.76-.98%202.27-.63.63-1.61%201.32-3.33%201.32-2.66%200-4.74-2.14-4.74-4.8%200-2.66%202.08-4.8%204.74-4.8%201.43%200%202.48.56%203.25%201.29l1.27-1.27c-1.08-1.03-2.51-1.82-4.53-1.82-3.64%200-6.7%202.96-6.7%206.61%200%203.65%203.06%206.61%206.7%206.61%201.97%200%203.45-.64%204.61-1.85%201.19-1.19%201.56-2.87%201.56-4.22%200-.42-.03-.81-.1-1.13h-6.07v-.01zm45.31%201.4c-.35-.95-1.43-2.71-3.64-2.71s-4.01%201.72-4.01%204.25c0%202.38%201.8%204.25%204.22%204.25%201.95%200%203.08-1.19%203.54-1.88l-1.45-.97c-.48.71-1.14%201.18-2.09%201.18s-1.63-.43-2.06-1.29l5.69-2.35-.19-.48h-.01zm-5.8%201.42c-.05-1.64%201.27-2.48%202.22-2.48.74%200%201.37.37%201.58.9l-3.8%201.58zm-4.62%204.12h1.87v-12.5h-1.87v12.5zm-3.06-7.3h-.06c-.42-.5-1.22-.95-2.24-.95-2.13%200-4.08%201.87-4.08%204.27%200%202.4%201.95%204.24%204.08%204.24%201.01%200%201.82-.45%202.24-.97h.06v.61c0%201.63-.87%202.5-2.27%202.5-1.14%200-1.85-.82-2.14-1.51l-1.63.68c.47%201.13%201.71%202.51%203.77%202.51%202.19%200%204.04-1.29%204.04-4.43V22h-1.77v.69zm-2.14%205.88c-1.29%200-2.37-1.08-2.37-2.56s1.08-2.59%202.37-2.59%202.27%201.1%202.27%202.59c0%201.49-1%202.56-2.27%202.56zm19.91-11.08v12.5h1.87v-4.74h2.61c2.07%200%204.1-1.5%204.1-3.88s-2.03-3.88-4.1-3.88h-4.48zm4.52%206.03h-2.65v-4.29h2.65c1.4%200%202.19%201.16%202.19%202.14%200%20.98-.79%202.14-2.19%202.14v.01zm11.53-1.8c-1.35%200-2.75.6-3.33%201.91l1.66.69c.35-.69%201.01-.92%201.7-.92.96%200%201.95.58%201.96%201.61v.13c-.34-.19-1.06-.48-1.95-.48-1.79%200-3.6.98-3.6%202.81%200%201.67%201.46%202.75%203.1%202.75%201.25%200%201.95-.56%202.38-1.22h.06v.96h1.8v-4.79c0-2.22-1.66-3.46-3.8-3.46l.02.01zm-.23%206.85c-.61%200-1.46-.31-1.46-1.06%200-.96%201.06-1.33%201.98-1.33.82%200%201.21.18%201.7.42a2.254%202.254%200%2001-2.22%201.98v-.01zm10.58-6.58l-2.14%205.42h-.06l-2.22-5.42h-2.01l3.33%207.58-1.9%204.21h1.95l5.13-11.79h-2.08zm-16.81%208h1.87v-12.5h-1.87v12.5z'%20fill='%23fff'/%3e%3cpath%20d='M20.75%2019.42L10.1%2030.72a2.876%202.876%200%20004.24%201.73l.03-.02%2011.98-6.91-5.61-6.11.01.01z'%20fill='%23EA4335'/%3e%3cpath%20d='M31.52%2017.5h-.01l-5.17-3.01-5.83%205.19%205.85%205.85%205.15-2.97a2.88%202.88%200%20001.51-2.53c0-1.09-.6-2.04-1.5-2.52v-.01z'%20fill='%23FBBC04'/%3e%3cpath%20d='M10.1%209.28c-.06.24-.1.48-.1.74v19.96c0%20.26.03.5.1.74l11.01-11.01L10.1%209.28z'%20fill='%234285F4'/%3e%3cpath%20d='M20.83%2020l5.51-5.51-11.97-6.94a2.89%202.89%200%2000-4.27%201.72l10.73%2010.72V20z'%20fill='%2334A853'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_204_2'%3e%3cpath%20fill='%23fff'%20d='M0%200h135v40H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)